When Should a Founder Actually Hire a Venture Lawyer?

A Founder’s Guide to Hiring Venture Counsel

I. Let’s Lower the Temperature

Let’s be real: nobody rolls out of bed thinking, “Today’s the day I get to hire a lawyer!”

You’re probably more worried about your runway, your next product launch, or whether AI is the only thing VCs care about this week.

Legal? It just feels like expensive, time-sucking overhead.

So let’s make this simple:

You bring in a venture lawyer right before you hit the point of no return: when things get real, and you can’t afford to mess it up.

Here’s how you know you’re there.

II. When It’s Too Early (Yes, That’s a Thing)

I have well-meaning founders come to me all the time, trying to do the right thing by hiring counsel at the very beginning, before they even have a company.

I usually tell them to keep me in the loop, but honestly, it’s probably too early for me to add real value.

Some signs that it may be too early to bring in a venture lawyer are:

You’re still testing the idea.

You have no sales.

You’re still a solo act.

You haven’t even thought about investors or partners.

At this stage:

Set up your company the right way (online tools or solid templates work just fine at this stage).

Keep ownership simple, clear, and written down somewhere you won’t lose it.

Build.

If you’re a solo founder obsessing over your cap table before you even have customers, you’re probably focusing on the wrong thing. But if equity comes up, jot down what you agree on in a shared document — nothing fancy, just something you can find later when it’s time to get a lawyer involved. Keep it informal, but don’t trust your memory.

(For newer readers: a cap table (or capitalization table) shows who owns how much of the company.)

That table does matter.

But probably not right now.

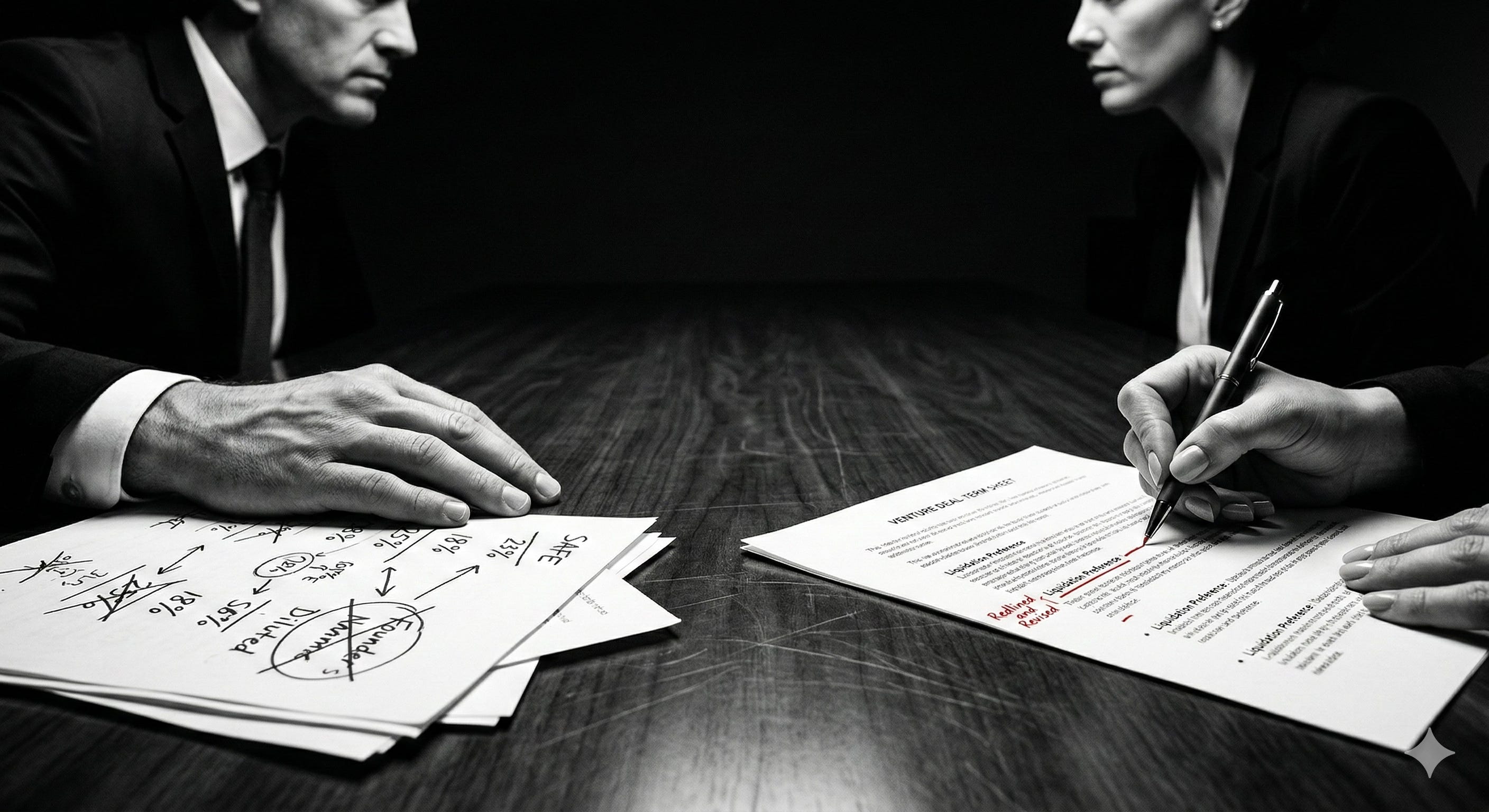

III. First Real Trigger: When Equity Stops Being Theoretical

You need a venture lawyer the moment you make promises that are hard (read: expensive) to unwind.

That includes:

Bringing on a co-founder.

Granting equity.

Issuing SAFEs.

Agreeing to board seats.

(For newer readers: A SAFE (Simple Agreement for Future Equity) is a common early-stage investment instrument. Investors give you money now in exchange for equity later, usually when you raise.)

Bringing on a co-founder isn’t just about splitting work. You need to think about setting legal terms and economic terms, and consider how to handle disagreements after the initial buzz fades.

Granting equity, issuing a SAFE, or agreeing to board seats all create permanent legal commitments for your company.

Even small mistakes can be expensive or impossible to unwind later. Getting counsel at this stage will help you protect your interests, memorialize control, and prevent surprises.

If you’re at any of these junctures, you shouldn’t DIY.

IV. The Asymmetry Rule: Experience Is Leverage

If you’ve somehow made it to the point where you’re across from a potential investor who has done 100 venture deals, while this is your first time at bat, it is time to hire counsel.

They might seem friendly, but they know this game inside and out. The negotiation isn’t on a level playing field.

Seasoned investors experience and negotiate things like:

Option pool expansions (setting aside shares for future employees — often increasing founder dilution if done pre-money).

Protective provisions (special investor rights that require their approval for major decisions).

Board composition (who actually controls governance).

All of these can shift power and control in your company in ways you won’t see coming.

If you don’t understand how they do those things, please don’t negotiate alone.

V. The Capital Threshold: Even “Small” Money Is Real Money

When you start bringing on capital, you should bring on counsel. And I don’t mean only when the seasoned investor from above comes knocking.

I’m talking about even when Uncle Bob wants to give you ten grand.

It’s common to take early money from friends and family, but doing so comes with risks.

If things go well, everyone is happy.

But if things get rocky (and let’s be honest, they usually do), unclear terms or handshake deals can turn into arguments, family drama, and legal difficulties.

Bringing in a lawyer early helps you put everything in writing, set expectations, and avoid misunderstandings that can wreck both your company and Thanksgiving dinner.

If you’re chatting with a potential investor and any of these words come up, take a break and get a lawyer:

Liquidation preferences.

Anti-dilution protections.

Board control.

Information rights.

Future fundraising flexibility.

Trust isn’t a substitute for clear documentation and a solid, professional foundation.

A little legal understanding now is way cheaper than cleaning up a mess later.

VI. The Underdog Reality: Geography Changes the Risk

If you’re building outside traditional venture hubs (whether that’s Cincinnati or somewhere else), you must understand these terms and partner with counsel before it is too late.

In underdog markets, capital is tight. That means:

You don’t get endless recapitalizations.

VCs from other markets may try to get terms heavily in their favor.

You’re fighting the “small market” stereotype every step of the way.

Bring in counsel at the right moment, then keep grinding.

VII. The Clean Framework: Know the Trigger. Act Deliberately.

When equity becomes real, lawyer up.

When capital comes knocking, lawyer up.

When your investment knowledge is outmatched, lawyer up.

Before those moments: grind and build.

After those moments, get strategic and intentional about your next moves — with the right experts in your corner.